How to Open a U.S. LLC

from Spain: The Definitive 2026 Guide

The guide your advisor doesn't want you to read.

Everything you need to know to create, operate, and protect your U.S. LLC as a foreign founder — taxation, taxes, bank account, IRS and the Spanish tax authority. No fluff.

Each year, thousands of digital entrepreneurs from Spain and Latin America open a U.S. LLC. Most do it blindly: they copy what they saw in a YouTube video, hire the first agent they find, and pray that the Spanish tax authority doesn't come knocking.

Mistake. A poorly set up U.S. LLC won't save you taxes — it'll multiply them. It'll get you into trouble with the IRS, the AEAT, or both. And when you realize it, you've already lost months and thousands of euros.

This U.S. LLC guide for Spaniards exists to prevent that from happening to you. You won't find academic theory or vagueness here. You'll find the complete operations manual — from step-by-step LLC creation to protecting your taxation with the Spanish tax authority.

📖 Before you start: This guide is extensive (~1-2 hours of reading). Consider it a reference manual: you don't need to read it all at once. You can go through sections as needed at any time.

Part of the content is public and another part is reserved for Devil Club members 🔒. Locked sections are automatically unlocked when you log in.

5 Phases. From zero to documented structure.

🧱 The Foundations

What is an LLC, why the USA, how it works, and myths to forget.

🔍 El Filtro

Is it right for you? Compatibility, ETBUS, the Manager, and the Operating Agreement.

💶 Your Money and Taxes

IRPF, VAT, US/Spain tax obligations, withdrawals, deductible expenses, and tax residency.

⚙ ️ Daily Operations

EIN, banking, accounting, privacy, and crypto post-DAC8.

This guide is constantly updated. Tax legislation changes, IRS rules evolve, and we keep this document up-to-date. If anything changes, you'll know here first.

Table of Contents

🧱 The Foundations: What is an LLC

- 🔑 What is an LLC? — Pass-through, Disregarded Entity and why it matters

- 🌍 Global Prominence — Why LLCs dominate the digital world

- ⚖ Legality and Economic Sense — Legal basis, advantages and transparency

- 💰 Economic Sense — Management, operations and strategy

- 🇺🇸 Why the U.S.? — The American advantage vs. Ireland and Estonia

- 🛡 Legal Shield — Limited liability and anonymity

- 📍 Recommended States — Delaware vs. Wyoming vs. New Mexico

- 🏛 Tax Classification — How the IRS sees you (Single vs. Multi-Member)

- 🧠 Disregarded Characteristics — What it means and how it works

- 💸 Pass-through and RAR — How LLC money flows to IRPF

- 🤝 Double Taxation Agreement — Spain-U.S.: what applies and what doesn't

- 📋 The Fine Print — IRS reporting nobody tells you about

- 💥 Debunking 5 Myths — What YouTube got wrong

- 🚫 What an LLC Doesn't Do — Brutal demystification: 7 uncomfortable truths

- 👻 🔒 Phantom Digital Protocol — Members only 🔒

- 📡 🔒 Tax Authority Radar (CRS/FATCA) — Members only 🔒

🔍 Compatibility and Requirements

- 🎯 Who is it for? — Ideal LLC entrepreneur profile

- ✅ Is your business compatible? — Exclusion list and interactive test

- 🎯 Real Use Cases — Freelancer, Agency, Infoproductor, E-commerce

- 🚩 ETBUS and Permanent Establishment — The line you shouldn't cross

- 🎯 Control vs. Ownership — Owner ≠ Manager: roles, governance, and substance

- 🔒 7 Fatal Mistakes — Client self-sabotage 🔒 Members only

- 🛡 The Manager (Your Proof of Life) — Economic substance for the tax authority

- 🔒 Legal Firewall — Breaking down the Manager's role 🔒 Members only

- 📜 Operating Agreement — Anatomy, structure, and key clauses

- 🔒 OA: Anatomy of Your Weapon — Clause-by-clause breakdown 🔒 Members only

💶 Taxes and the Tax Authority

- 🏛️ IRPF and Income Attribution — How your LLC income is taxed + Calculator

- 👾 99% Hack — Solution to the Modelo 100 bug 🔒 Members only

- 💸 Withdrawals and Deductible Expenses — What you can and can't deduct

- 🇪 🇺 European VAT — B2B, B2C, OSS, and the VAT MOSS trap

- 📢 85K Directive — The VAT franchise Spain refuses to apply

- 🇺🇸 Obligaciones USA — 5472, 1120, Sales Tax, FBAR, BE-13C

- 📄 Form 1099 — What it is, when it applies, and when it doesn't

- 🇪 🇸 Spain Tax Obligations — Modelo 720, 100, 130

- 💣 Modelo 184 — The multi-member LLC bomb

- 👷 RETA and Self-Employed Workers — When required, when not

- ✈ ️ Tax Residency and CFC — Tax residency and CFC structures

- Failure Points — Where a "perfect" LLC breaks down 🔒 Members only

- 🌍 LLC by Country — Compatibility map by tax residency

- 🗓️ EIN Timeline → Bank — Step-by-step from scratch

- 🏦 Recommended Banks — Mercury, Wise, Revolut + comparison

- 💸 Hidden Costs — Currency conversion, maintenance, what nobody tells you

- 📊 Accounting — What's required and what's not

- 📑 Simple Accounting Sheet — LLC accounting 🔒 Members only

- 🎬 A day with your LLC — Real-life simulation of day-to-day

- 🕵️ Post-DAC8 Privacy — Members only 🔒

- 🪙 Post-DAC8 Crypto Protection — Members only 🔒

😈 Pricing and Opening Process

- 🗺️ Hoja de Ruta + Timeline Realista — 4 pasos + semana a semana

- 💵 Flat Fee — What's included (with/without manager)

- 📦 Deliverables — The 8 pieces you receive

- 🔍 Checklist: Good Provider — What to require and what to never accept

- ⚔️ Solo vs. Devil Club — La comparativa honesta

- 🏛 LLC + SL — Can they be combined?

- ™ Intellectual Property — Protect your brand with LLC

- 🛡 Insurance — Do you need one?

- 🚪 Dissolution — Closing your LLC properly

🧱 The Foundation: What is a U.S. LLC and Why Create One

What the Spanish tax authority doesn't tell you and your buddy won't either. Understand the legal basis to sleep tight.

🔑 What is a U.S. LLC? (Pass-through and Disregarded Entity)

Let's start with the fact that LLC stands for Limited Liability Company, or "Limited Liability Company". These are very popular and flexible legal business structures for many digital businesses or freelance professionals.

Why? Because they offer the best of both worlds: limited liability (like a corporation) and flexible management and taxation (similar to a self-employed worker or partnership), but with fewer formalities.

🔑 Key Concept: "Pass-Through" (Transparency)

In many cases, LLCs function as «pass-through» entities. This means that the profits generated at the end of the year are directly attributed to their owner and must be reported on their personal tax return, such as their the Spanish tax authority's IRPF or equivalent, depending on their tax residency.

You can't accumulate profits indefinitely without being taxed. That's why LLCs are designed to invoice, spend, and be taxed in an orderly fashion.

Another advantage is that LLCs don't need a board of directors or mandatory annual meetings, which simplifies their management. This is especially attractive to small businesses or solo entrepreneurs.

The so-called "pass-through taxation" means that the LLC's profits and losses are passed on to the personal tax return of the member or members, avoiding double taxation that affects corporations.

It occurs when a company pays taxes on its profits in the country where it's registered and then its owners pay taxes again in their country of fiscal residence on the dividends they receive. This system can generate a high tax burden. LLCs avoid this problem by being taxed only once (at the owner's level).

🌍 Why the American LLC dominates global digital business

The LLC isn't a modern "loophole" or a glitch in the Matrix. It's a proven tool.

It was born in Wyoming in 1977. It was a radical innovation designed to combine the best of two worlds: the bulletproof protection of large corporations and the tax agility of personal partnerships.

In the 90s, the U.S. adopted this model. Today, it's the gold standard for digital commerce.

Why do Silicon Valley startups and global freelancers use the same structure? For three market-breaking advantages:

⚖ Is it legal to open an LLC in the U.S. as a Spaniard?

Spoiler: Yes. But only if you understand the rules of the game.

If you're a tax resident in Spain, creating a LLC (Limited Liability Company) in the U.S. is one of the smartest legal forms available. It allows you to own a foreign company without legal or tax issues, as long as you declare what's owed.

📈 Benefits for your business

- Pass-Through Efficiency: The LLC doesn't pay corporate taxes (like Spain's Corporate Tax). Profits pass directly to the owner, who reports them on their personal tax return. No double taxation.

- No Spanish Regulations: Without a Permanent Establishment in Spain (if you meet the rules), you avoid local bureaucracy, corporate social security contributions, and quarterly VAT.

- Global Market: Operate without geographic borders. Ideal for digital services, SaaS, or international e-commerce.

👁 Transparency vs. Privacy

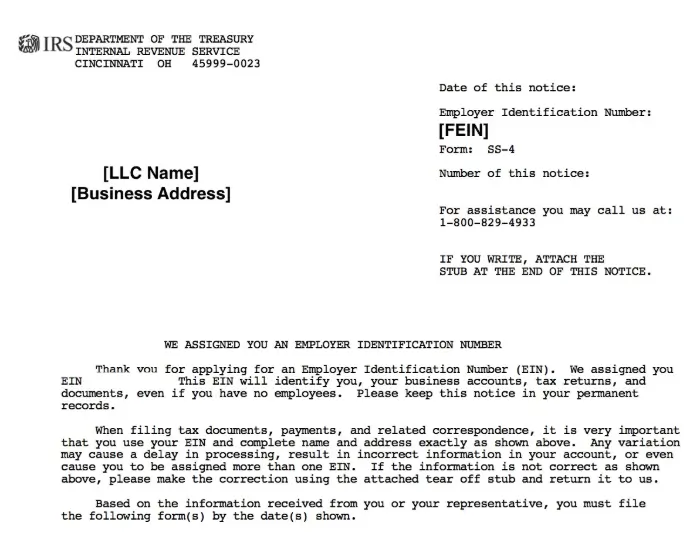

🚨 CRITICAL OBLIGATION: Form 5472 and 1120

If you own more than 25% of a foreign LLC, you must report transactions between you and the LLC to the IRS each year.

The Penalty: Automatic fines of up to $25,000 for not filing or filing incorrectly.

(Don't worry: our flat fee includes filing for you).

🚫 «You can do it yourself, it's easy» — the WhatsApp group is lying

Whenever someone asks about U.S. taxes in an entrepreneur group, the self-proclaimed expert shows up and tells you to do it yourself. This conversation — with names changed — is real:

If you don't know what any of those four things are, you're one CP-215 away from discovering that "easy" costs $25,000. 13:17 ✓✓

Filing Form 5472 yourself seems like a good idea until you see what's inside the form. Three reasons you shouldn't:

🎓 No PTIN = illegal

The IRS requires anyone getting paid to prepare a return to have a PTIN (Preparer Tax ID Number). Your Spanish accountant cousin doesn't have one. Neither does that $30 Fiverr gig. If they sign without a PTIN, it's fraud; if they don't sign, you're fully responsible to the IRS.

🧩 TurboTax does not do 1120 pro-forma

No consumer software (TurboTax, H&R Block, FreeTaxUSA) supports the 5472 + 1120 pro-forma combo for foreign-owned SMLLCs. It requires professional software or manual preparation on paper, then certified mail or fax.

👥 Related Parties olvidadas

Form 5472 requires reporting every transaction with related parties: yourself, your holding company, your spouse, other LLCs. 95% of DIY filers omit this. The IRS cross-references data with banks via FATCA/CRS. Base penalty: $25,000.

💰 Advantages of Forming an LLC: Economic and Tax Sense

Choosing a U.S. LLC is a strategic decision. We seek operational efficiency and a solid legal framework globally.

Flexibilidad Total

As a Single-Member Disregarded Entity, you control operations without partners or complex structures. You adapt to the fast digital market without bureaucracy.

Limited Protection

Your personal assets are protected from debts or lawsuits. The LLC creates a clear firewall between your finances and the business.

Privacidad en el Registro

Some states (NM, WY) allow you to keep your name private. You protect your business identity while still complying with the tax authority.

Contabilidad Simplificada

As a pass-through entity, you don't file complex annual accounts. Income and expenses flow directly through. Less paperwork, lower costs.

Costes Eficientes

Formation and maintenance are very cost-effective. No large upfront expenses, making it easier to get started.

Reduced Bureaucracy

Fewer forms and regulations. Focus on growth, not filling out PDFs for administration.

Access to Stripe USA

Better rates, more integrations, and services than the European version. Ideal for info-products and SaaS.

Access to the US Dollar

Stability against local volatility. A strong currency for international negotiations.

Top Banks

Top-tier products, multi-currency accounts, and easy international payments.

Investment & VCs

More attractive to foreign investors. If you're seeking funding, being in the U.S. makes a difference.

Entorno Legal Favorable

Clear laws, small business incentives, and robust intellectual property protection.

Global Reputation

Having an American company carries weight. It conveys trust, professionalism, and seriousness.

Internationalization

Sell to the world with ease. The network of trade treaties works in your favor.

🇺 🇸 U.S. LLC vs. Company in Ireland, Estonia or Dubai

The United States is more than just Hollywood. It's an administrative paradise for global entrepreneurs. The LLC was created to help modest self-employed workers, but it has evolved to be used by everyone from freelancers to million-dollar empires.

🏆 The American Advantage

- Economic and Fast: Set up in days, not months. Maintenance costs are ridiculously low compared to Europe.

- 100% Remote: Create and manage your company without setting foot in the U.S.

- Scalability: Suitable for invoicing $10,000 or $10 million.

⚠ BUT... IT'S NOT THE ONLY OPTION (COMPARATIVE)

🇮🇪 Irlanda (La Corporativa)

- Corporate Tax: 12.5% (Low, but you pay).

- Market: Total access to the EU.

- ❌ The Barrier: Requires at least one EU resident director. Higher bureaucracy and costs.

🇪🇪 Estonia (La Digital)

- Digitalization: 100% online with e-Residency.

- Taxation: 0% if you reinvest (Deferral).

- ❌ La Barrera: Pagas 20% al repartir beneficios (no es Pass-Through puro como la LLC).

Singapore, Hong Kong, and Cyprus are also options, but for a Spain resident, they often add complexity (CFC rules, gray lists, etc.).

🚀 9 Strategic Reasons to Choose an LLC

Forming an LLC (Limited Liability Company) can be a good option for digital entrepreneurs and businesses looking to optimize their structure for global expansion and efficiency. Here are the key reasons to consider this legal form:

Here's what you gain in practice:

🛡 Limited Liability and Anonymous LLC: Your Legal Shield

Protection isn't magic. To maintain it, you must respect the separation between business and personal finances. You'll lose protection if:

🕵 The Superpower of Anonymity (Anonymous LLC)

In Spain, anyone can find out who owns an S.L. or where a self-employed worker lives with a simple search. In the U.S., states like New Mexico, Wyoming, or Delaware allow you to register an LLC without your name appearing in public records.

An anonymous LLC is a company registered in states like New Mexico, Delaware, or Wyoming, where the owner's name doesn't appear in public records. This extra layer of privacy can be very useful in sectors like cryptocurrencies, cybersecurity, or brand protection, where strategic anonymity is an asset.

But be aware: registral anonymity doesn't exempt you from your tax obligations as a Spanish resident. This is where many people get confused…

What Anonymity DOES Do

- Hide your name in public databases of the state where the LLC is registered.

- Make casual searches or unofficial tracking of ownership more difficult.

- Give you an advantage in markets where privacy is a valuable asset.

What Anonymity DOES NOT Do

- Doesn't eliminate your obligation to report LLC income on your Spanish tax return if you're a Spanish tax resident.

- Doesn't allow you to deduct personal expenses as business expenses (groceries, rent, vacations…).

- Doesn't protect you from the Spanish tax authority if you make unsubstantiated transfers between your LLC account and personal accounts in Spain.

So, is it worth it?

Yes, it serves to protect your privacy, not to hide income. A well-used anonymous LLC:

- Allows you to operate discreetly.

- Protects your business strategy and image.

- Strengthens your positioning in niches where confidentiality matters.

That's right, as long as you correctly declare your income and comply with your tax obligations as a Spanish taxpayer.

🔒 Protocolo «Fantasma Digital»

🧰 Your Tactical Arsenal (Direct Access)

- Namecheap: Dominio + Email

- Tello Mobile: USA phone number

- VPN Premium: Residencial

- Mercury Bank: USA banking

🛠 Secure Setup Strategy

Keys to avoiding rookie mistakes:

- Tello: Activate with eSIM using WiFi.

- Namecheap: Always enable «WhoisGuard».

- Mercury/Relay: Choose «Checking Account». 0% Interest = 0 Alerts.

📍 Best state to register your LLC: Wyoming vs. Delaware vs. New Mexico

Not all states are created equal. Some are for giant corporations and others for smart entrepreneurs. Out of 50 states, these three are the top contenders for your LLC.

👔 Delaware

«El favorito de Wall Street»

Standouts for their legal security and sophisticated legal framework. Ideal for attracting investors and customizing complex structures.

🤠 Wyoming

«The original bunker»

Offers solid asset protection, limiting creditors' reach. No state corporate or personal income taxes.

Shines for its administrative efficiency. Fast, no Annual Report required, and minimizes management. Keeps your name out of the public record by default.

- ✓ Lowest cost.

- ✓ Zero annual paperwork.

- ✓ Full privacy on the registry.

⚠ What happens after forming your LLC (and nobody tells you)

Most providers give you formation papers and disappear. But forming an LLC is only 20% of the work. This is what you need to actually operate:

| Necesidad | Formacion low-cost | Devil Club |

|---|---|---|

| Permanent Registered Agent | Extra ($125–$299/yr) | ✓ Always included |

| Annual tax filing (5472 + 1120) | Find a CPA ($200–$500) | ✓ Included with wizard |

| Bookkeeping / accounting | Find a bookkeeper ($150+/mo) | ✓ Integrated with your bank |

| Compliance (FBAR, BEA, BE-13) | Nobody warns you it exists | ✓ Automatic |

| Substance before the Tax Authority | No considerado | ✓ Gobernanza documentada |

| Soporte en Spanish | No disponible | ✓ WhatsApp/Telegram + Lucy IA |

🏛 How the IRS classifies your LLC: Single-Member vs. Multi-Member

The IRS (Internal Revenue Service) is the U.S. tax agency. They see you differently if you're solo versus with partners. This is where your tax future is decided:

👤 Single-Member LLC (Unipersonal)

- The IRS considers it a «Disregarded Entity».

- Invisible: La LLC no «existe» a efectos fiscales federales.

- Transparent: You're taxed as a self-employed worker, but in your country of residence (Spain).

👥 Multi-Member LLC

By default, the IRS treats it as a Partnership.

- Members report their share of profits.

- Requires complex informational returns (Form 1065).

📄 Corporation Option: You can elect to be treated as a C-Corp (Form 8832).

⚠ Danger: The LLC pays taxes and you do too (dividends). Double taxation.

- No U.S. employees.

- No need to have a physical office in the U.S.

🧠 LLC Disregarded Entity: What it means and how it works

When an LLC has a single owner and hasn't elected to be taxed as a corporation, the IRS classifies it as a Disregarded Entity.

🧠 What does 'Disregarded' mean?

For you, as a tax resident in Spain, this implies two parallel realities:

🇺🇸 En EE. UU.

If you're not an ETBUS (no physical presence), you don't pay federal tax.

But you do fulfill reporting obligations: Form 5472 + pro-forma 1120 each year.

🇪 🇸 🇪🇸 In Spain

Profits are considered foreign attributed income (RAR).

They are taxed in your IRPF (General Base or Savings, depending on the activity).

🚧 Limitations to Consider

Despite its advantages, this structure has restrictions:

- No partners allowed: It's «Single-Member». If you want formal partners, the rules change (Partnership). But note: even if the LLC has only one member, the Operating Agreement allows structuring payments to third parties — via service contracts, intellectual property licenses, or profit-sharing agreements. You own 100% of property, but profits can flow to collaborators through legitimate operating expenses, without adding members or changing tax structure.

- Double Compliance: You must file paperwork in the U.S. (informational) and in Spain (tax-related). This adds some administrative burden.

Main Characteristics:

So, before choosing this structure, make sure it aligns with your goals. (Spoiler: If you're a digital freelancer, it's often a great fit).

💱 How an LLC is taxed on the IRPF: Attribution of Income Regime

In practice, the pass-through turns the LLC into a tax channel: what enters the company, the Tax Authority considers it yours that same year. Your role is to document each figure and maintain impeccable order.

💸 The Case of €50,000:

Imagine your LLC earns €50,000 in net profits. As a pass-through entity, that €50,000 directly adds to your personal taxable base in Spain.

This means you'll declare the full amount on your IRPF as foreign-attributed income, applying the applicable tax bracket according to the tax authority's scale for that year.

📍 Where and why it's taxed

- 🇪 🇸 🇪🇸 Spain (IRPF): You are taxed via RAR, applying the IRPF brackets and rules corresponding to your case.

- 🇺 🇸 🇺🇸 U.S.: Federal tax only applies if ECI/ETBUS exists. If not, you don't pay tax there, but you report (5472 + 1120 pro-forma).

📊 How it integrates into your IRPF (Practical Keys)

- Naturaleza de la renta: El RAR mantiene la naturaleza original.

- If you sell services/infoproducts → Foreign Economic Activity Income (General Base).

- If you earn interest/dividends → Capital Investment Income (Savings Base).

- Conversion to euros: Use the official exchange rate on the accrual date or the annual average exchange rate from the Bank of Spain.

⚠ Common mistakes that cause problems:

🇵🇾 And in Paraguay? In Paraguay, there is no Income Attribution Regime (RAR). With a territorial regime, the benefits of your LLC (foreign source) are taxed at 0%. No automatic imputation: you only pay IRP (10%) on what you distribute locally. No fictitious income, no forced pass-through. Explore residency change →

🔄 Flujo de Caja & Fiscalidad

🇵🇾 And in Paraguay? In Paraguay, the territorial regime eliminates automatic attribution. Your LLC's profits are only taxed if you distribute them locally (10% tax). No forced distributions, no progressive tax, no Form 100. The money left in Mercury is 100% yours. Explore residency change →

🤝 Spain-US Tax Treaty and Your LLC

Spain and the U.S. have a tax treaty to prevent citizens and companies from paying taxes twice on the same income.

🎯 Objetivo

The treaty sets clear rules on where and how much you pay in taxes, promoting trade and investment. Basically, it prevents the Spanish tax authority and the IRS from fighting over your money.

💰 Beneficio Principal

If you've already paid in one country, you won't pay in the other. You can deduce what you paid in the U.S. from your Spanish tax bill.

🧠 How does it work in practice?

Think of it like being a citizen of one country and earning money in another. This agreement tells you that you might not have to pay taxes in the country where you earned that money.

- If you're Spanish and earn money in the U.S., you might not have to share your profits with the U.S. government.

- This agreement also eliminates double taxation on dividends, interest, and royalties.

📋 Tax Obligations of Your LLC You Didn't Know About

Who Do You Report To?

Running a U.S. business while living in Spain is a balancing act:

- One Wants Your Money: the Spanish tax authority wants to collect on your global profits.

- The Other Wants Your Data: The IRS doesn't want your taxes (if you do it right), it wants your financial information.

The Deal? The U.S. lets you operate tax-free in exchange for using its currency (the Dollar), consuming its services, and providing market intelligence on your global business.

🇪🇸 Tax Authority (Spain)

Your Obligation: PAY.

If you reside more than 183 days per year here, you're a tax resident. You must report and pay taxes on your U.S. business profits (via IRPF).

⚠ Your tax rate depends on your personal situation.

🇺🇸 IRS (EE. UU.)

Your obligation: REPORT.

Even if you don't pay taxes there (no office or employees), you must be transparent with the Internal Revenue Service.

- Form 5472 + 1120: Mandatory annual report.

- Philosophy: 'You only report there, but information is power.'

☠ Consecuencias de Incumplir

Our goal isn't to scare you; it's to help you understand why you must act within the legal framework. If you play by the rules, you win. If you improvise, you lose.

📋 Your 5 Commandments (Responsibilities)

🇵 🇾 🇵🇾🇺🇸 And in Paraguay? In Paraguay, your obligations are drastically reduced: you only comply with the IRS (5472+1120) and submit your annual IRP to the DNIT (a single declaration). No Modelo 720, no 100, no 130, no 184. The DNIT does not have an aggressive automatic exchange with the US like the AEAT. Explore changing your residence →

🚨 COMMON ERRORS AND RISKS

⚠ It's crucial to understand the responsibilities of operating an LLC. Lack of knowledge or non-compliance can lead to significant risks. Our goal is to help you understand why you must always act within the legal framework to prevent unnecessary consequences. Key responsibilities to keep in mind:

🔑 How to sleep tight

- 📂 Transparency: Maintain clear records and document all financial operations.

- 🔗 Coherence: Align your LLC's activity and structure with your tax residence and applicable laws.

- 🧠 Expert Advice: International taxation is complex; having a qualified professional ensures your strategy is legal and tailored to your situation.

🔒 How do they catch you? The Tax Authority's Radar (CRS/FATCA)

📡 The 4 Attack Vectors

The Mistake: Opening an account for your LLC in a European fintech (Wise Europe, Revolut Business LT/BE, Qonto, etc.).

The Radar: These entities are UNDER CRS (Common Reporting Standard) regulations. Even if your company is U.S.-based, if you have a euro IBAN, it's in Europe, and the bank will automatically report the balance to the tax authority if it detects you're a resident there, especially with DAC8.

The Mistake: Using your LLC's card for daily life in Spain (Mortgage, Water or Services, Gym, Amazon ES, Internet).

The Radar: If the Spanish tax authority cross-references data and sees a foreign card paying recurring expenses of a tax resident, you've created a physical and traceable link between your LLC and yourself. Boom! Effective address demonstrated and attribution of all unreported income.

The Mistake: Telling your structure to someone you shouldn't or having intimate enemies.

The Radar: An angry ex-partner in a contentious divorce or a business partner you fired. This is the #1 source of "anonymous" inspections. Discretion is your best asset.

The Mistake: Putting 'CEO at [Your LLC's Name]' on LinkedIn or Instagram, while being geolocated in Spain.

The Radar: Inspectors use Google. If you publicly identify yourself as the director of a foreign company and don't report anything on the Modelo 720 or IRPF, you're putting a target on your back.

The U.S. DID NOT sign the CRS. It signed the FATCA. This means:

- The world sends data to the U.S. (FATCA).

- The U.S. DOES NOT automatically send data to the world (except in cases of severe fraud or terrorism).

- If your money is in a 100% U.S. bank (Mercury, Relay) and you don't generate interest (to avoid Form 1042-S), you're digitally invisible to the European automatic radar.

💥 Debunking Myths: «Not taxed without distribution», «It's Illegal», «Leaving it at 0», «$18,000 Deduction», and «Invisibility»

The internet is full of "gurus" recommending magic tricks. Be careful: what works in a TikTok video can be a crime in real life. Let's debunk the 3 most dangerous myths with the law in hand.

The "Technically..." Myth ("If I don't bring the money, I don't get taxed")

This is the most sophisticated and dangerous myth. It's based on a very attractive theory that goes like this:

"If your LLC is a Foreign-Owned Disregarded Entity, U.S. law doesn't 'attribute' the income to you, it only requires you to 'report' it. Therefore, in Spain, you only get taxed on the money you actually withdraw (distributions)." — Internet snake oil salesmen 💨

It's the famous "technically..." thesis. Its foundation is a literal interpretation of IRS forms.

🛑 THE REALITY (The Tax Authority's Hammer):

Although the technical defense is clever, it crashes against the principle that the tax authority systematically applies: Economic Reality.

- Who gets the income? You.

- The company pays taxes? No (it's pass-through).

Inspector's conclusion: The benefit is yours from the moment it's generated. For the tax authority, your LLC being disregarded is the definitive proof of its total transparency, not a shield of opacity.

For 99% of entrepreneurs, the aggressive approach doesn't compensate for the stress or the cost of defense. Peace of mind is priceless.

🛡 Via Conservadora («La Fortaleza»)

- Declare 100% of annual profits on your income tax return via RAR.

- Face higher short-term tax costs.

- SANCTION RISK: ZERO*. Sleep tight.

*As long as everything is properly documented.

⚔ Via Agresiva («Guerra de Guerrillas»)

- Only report distributions (what you withdraw).

- Exige defensa impecable: Manager en USA, actas, evidencia de actividad corporativa real…

- LIKELY OUTCOME: Audit, lengthy and costly litigation.

«It's a Tax Haven and It's Illegal»

This is fear #1. You've probably heard this urban legend at a holiday dinner or online forum:

🛑 THE REALITY (the U.S. isn't a pirate island):

⚖ Your 2 Shields of Legality:

1. La DGT lo reconoce

The Spanish Tax Authority has confirmed in binding consultations that LLCs are valid and transparent ('pass-through') entities that must be taxed in the partner's IRPF. (This isn't a loophole; it's regulated).

2. El Convenio Fiscal

The U.S. and Spain have a Double Taxation Agreement since 1990. This treaty exists to facilitate doing business in both countries without paying taxes twice on the same income.

🧠 THE DIFFERENCE BETWEEN LEGAL AND ILLEGAL:

'If I empty my account at the end of the year, I don't pay taxes'

If you've searched 'how to avoid paying taxes with an LLC' online, you've probably come across this 'tax engineering' advice. It's the most common trap.

🛑 THE REALITY (the tax authority isn't stupid):

Taxation doesn't look at your bank balance on New Year's Eve. It looks at your annual flow (Actual income - deductible expenses).

If you invoice €50,000 and spend €50,000 on personal things, to the tax authority your profit is still €50,000… and they'll penalize you for not declaring it.

⚠ THE DANGER: «Tax Simulation»

If you «empty» your account by spending on personal vices (clothing, leisure, housing) and pass them off as business expenses, you're committing fraud. If you can't document that these expenses generated income for the business, you're exposing yourself to an inspection and sanction.

When does this strategy work? (The Legal Way)

Having zero profit is perfectly legal if it's real. This means you've reinvested all income in business growth through permitted expenses.

✅ IF YOU CAN DEDUCT:

- Software and tools.

- Advertising and Marketing.

- Freelancers and staff.

- Specific training.

❌ IF YOU CAN'T DEDUCT:

- Personal purchases.

- Rent/Electricity at your home.

- Offices in Spain (EP!).

- Salaries in Spain.

«Can I deduct $18,000/yr for remote work?»

Some «LLC sellers» claim you can deduct up to $1,500/mo for working from home.

🛑 THE REALITY (we wish):

Let's break it down:

🇺🇸 In the United States

- The actual deduction is $1,500/YR.

- Only applies if you're taxed there (Self-employed).

- Doesn't apply to you: As a Disregarded entity and being taxed in Spain, this rule doesn't affect your IRPF.

🇪🇸 In Spain

- Only deductible if you're a Self-employed worker and have exclusive space.

- ⚠ HIGH RISK: If you allocate part of your home to the LLC, you may create a Permanent Establishment (PE).

- That complicates your tax situation.

«The Spanish tax authority can't see what I have in the U.S.»

This is the «Ostrich» myth. Many believe physical distance equals tax invisibility. The idea is that if the bank server is in New York or on the Blockchain, the Spanish tax authority's binoculars can't reach there.

🛑 THE REALITY (Yes and No):

It's true: the tax authority doesn't have a real-time «window» into your Mercury account in dollars. But the noose is tightening.

The Spanish tax authority is blind in the U.S.… until it's not. A single cross-border transfer to a Spanish account, a card payment with your name on it, or a random inspection of your foreign assets can unravel everything.

🚨 2025 UPDATE: The DAC8 Directive

Don't feel safe in 'limbo.' With DAC8, the European Union requires the automatic exchange of information on:

- Cryptoassets: Anonymity is over for centralized exchanges based in Europe.

- Electronic Money (E-money): If you hold balances in Euros (€) on European-based platforms and banks, it's easier for alarms to go off.

🚫 What a LLC Doesn't Do: 7 Things Nobody Tells You

Before we proceed, let's take a step back. A LLC is a powerful tool, but it's not magic. If someone sold you on these ideas, they lied:

- It doesn't eliminate taxes. You still pay taxes in your country of fiscal residence.

- It doesn't make you invisible to the tax authority. There are cross-border reporting obligations.

- Doesn't change your tax residency. You live in Spain = you pay taxes in Spain.

- No personal expense deductions as if they were business expenses.

- Doesn't automatically shield you from RETA if you provide personal services.

- Not an offshore account to hide money. That's a crime.

- Doesn't work on autopilot. Requires annual maintenance, compliance, and filings.

- Separates your personal and business assets (limited liability).

- Gives you access to US banking, payments, and tools.

- Reduces total tax burden if structured correctly (deductible expenses).

- Generates economic substance outsifrom Spain with a Manager.

- Allows invoicing in USD to global clients without being self-employed in Spain (RETA gray area).

- Offers commercial anonymity (NM doesn't publish the owner).

- Simplifies operations vs. an SL: no notary, no minimum capital, no intra-community VAT.

🔍 The Filter: Is Your Business Compatible with an LLC?

🎯 Who Benefits from Opening a U.S. LLC? Digital Entrepreneur Profile

If you're a digital entrepreneur in Spain (or living outside Europe) working with clients worldwide, there's a legal structure that can become your best ally: the LLC.

Optimize your management, pay fewer taxes legally, and document your personal wealth. All in a flexible format designed for global businesses.

Not everyone fits with an LLC. But if you see yourself in one of these 6 profiles, you're likely losing money and peace of mind by not having one:

But be careful: it's not a universal solution. Before taking the step, you must understand your tax and legal obligations.

💡 A solid structure can be the difference between a business that grows unencumbered and one that gets bogged down in unnecessary taxes and paperwork.

✅ Businesses compatible with an LLC: Complete list of activities

While LLCs offer a flexible and highly attractive structure for digital entrepreneurs, their suitability really depends on the nature of your activity and your tax residence. To operate with full legal certainty, it's crucial to understand which business models are truly compatible with an LLC under U.S. law and the law of your country of residence.

In the case of Spain and the U.S., only certain types of activities can fully leverage this vehicle. The golden rule is twofold: avoid generating a permanent establishment in Spain and don't fall into the ETBUS (Engaged in Trade or Business in the U.S.) category on U.S. territory.

🌳 Arbol de decision rapida

👇 Search your specific activity in the interactive detector

🧭 LLC Compatibility Detector

Search your activity to see if you can operate without a Permanent Establishment in Spain.

| Activity | Verdict | Quick Analysis |

|---|

A LLC on its own isn't your definitive solution, but you can use Combined Strategies:

- 🏢 Use an SL or Self-Employed Worker for the physical/in-person part in Spain.

- 🇺🇸 Complement with an LLC for digital areas, marketing, or international expansion.

*This way, you separate risks, optimize taxation for the digital part, and comply with local regulations.

Related Operations: Transparency and Compliance

When two related companies (e.g., with the same owner) conduct transactions with each other, these are considered related-party transactions. It's essential that these transactions are conducted with total transparency and legality to ensure regulatory compliance.

Tax regulations state that related-party transactions must be valued at arm's length prices, i.e., at the price that would have been agreed upon between independent parties in free competition. This principle aims to ensure that profits are correctly allocated to each entity, preventing artificial profit shifting for tax purposes.

Invoices must correspond to services actually rendered or goods actually delivered.

The agreed-upon prices must be consistent with those that would apply between unrelated companies.

It's crucial to have detailed contracts, valuation reports, and proof of actual service performance or goods delivery. This is essential to justify operations to the Spanish tax authority.

💡 Recommendation: Always conduct related-party transactions with maximum transparency and at market prices. Consult with a tax advisor specializing in international taxation to ensure correct compliance.

🎯 Real use cases: 4 profiles that successfully use LLCs

Not all digital businesses use LLCs the same way. Here are 4 real profiles of entrepreneurs operating with American LLCs, with the particularities of each model:

Profile: Developer, designer, copywriter. Invoices US/EU clients. Receives USD via Mercury.

LLC Advantage: Invoices without being self-employed (gray area under RETA), receives dollars, deducts tools and software.

Risk: If you personally provide services > €30K/year, RETA is likely.

Profile: Marketing, development, or consulting agency with a remote team. Contractors in Latam/Asia.

LLC Advantage: Pays contractors in USD without friction, centralizes international invoicing, scales without country limits.

Risk: If you have employees in Spain, EP is automatic. Contractors yes, employees no.

Profile: Sells online courses, mentorships, templates. Global audience. Uses Hotmart, Gumroad, Teachable.

LLC Advantage: Marketplaces (Hotmart, Gumroad) manage VAT for you. Passive income does not generate habitual RETA.

Risk: One-on-one mentorships if they are personal services. Recorded courses, no.

Profile: Sells digital or physical products (dropshipping, print-on-demand, SaaS). Stripe/Shopify as a payment gateway.

LLC Advantage: Native US Stripe account, no Stripe Atlas limits. Platform expenses are deductible.

Risk: Sales Tax if you exceed the threshold in states with a limit. B2C to EU = destination VAT (use MoR or OSS).

🚩 ETBUS and Permanent Establishment: The red lines of your LLC

To operate legally from Spain without being taxed in the U.S. or considered a disguised Spanish company, you must respect two key concepts. These are your two red lines. If you cross them, you'll get burned.

The Rules of the Game (Red Lines) 🚩

Avoid the following to prevent issues with your LLC:

🚩 1. DON'T be an "ETBUS" (To avoid US taxes)

The term ETBUS (Engaged in Trade or Business in the United States) is the IRS criterion to determine if your activity is sufficiently connected to the US, requiring you to pay federal taxes there. It depends not only on your physical location but also on whether your business has a presence or means in US territory.

Even if your LLC is a disregarded entity (taxed in your name, not the company), it may be considered ETBUS if certain criteria are met, generating federal tax obligations.

🚫 IF I'M ETBUS I pay US taxes

- 🏢 Real Physical Presence: Office, warehouse, employees, or managers living there.

- 🤝 Dependent Agents: People in the US with the power to sign contracts on your behalf.

- 📈 "Connected" Income (ECI): Sales generated directly by your physical structure there.

✅ I'M NOT ETBUS 0% US taxes

- 🌍 100% Remote Management: You operate from Spain. No office or employees on U.S. soil.

- 📦 Externalized Logistics: You use Amazon FBA or 3PLs. They handle shipping, you just give the order.

- 💻 Digital Sales / Services: The server may be in the U.S., but your "brain" (you) is outside.

- You must file a U.S. tax return.

- You'll pay federal taxes on U.S.-connected income.

- You might even need to file Form 1120-F (even if you're disregarded).

👉 If you sell digital services from outside the U.S., chances are you are NOT an ETBUS.

👉 As long as you don't have a physical presence or specific U.S. source income, you won't have tax obligations there beyond informational forms (like 5472).

Note: ETBUS isn't the only criterion that can affect your U.S. taxation. Factors like entity type, tax treaties between your country and the U.S., and applicable deductions or credits also matter. Before making a move, consult a tax advisor who knows the American market.

🚩 2. Don't have a "Permanent Establishment" (To avoid being an S.L.)

Your LLC is American by birth, but it can become Spanish through "contagion." If you cross this line, the Spanish tax authority will treat it as an S.L. and require everything (IS + VAT).

"A foreign entity has a Permanent Establishment in Spain if it has a fixed business location (office, premises) or acts through an authorized dependent agent who can contract on its behalf."

☠ Generas EP si…

- You Have a Physical Office: A premises, warehouse, or coworking space paid for by the LLC in Spain.

- You Have Payroll: You hire salaried employees in Spain in the LLC's name.

- You're a "Dependent Agent": You sign contracts in person or regularly negotiate with clients in Spain on behalf of the company.

✅ You're safe if…

- You're 100% Digital: Your infrastructure is in the cloud (servers, SaaS), not on Spanish soil.

- Freelancer Use: You contract B2B services (invoicing), not employees (payroll).

- Remote Management: Operations aren't tied to a fixed location here.

If you don't have a PE, the LLC doesn't exist for Corporate Tax. It becomes transparent.

You pay taxes (IRPF), but the company pays nothing. No corporate VAT, no Corporate Tax, and no local accounting

⚠ The Threat: Effective Management

🇺 🇸 🧠 Even if your LLC is registered in 🇺🇸 the U.S. and has no permanent establishment in Spain, understand the scope of effective management . This criterion only matters when the entity is taxed on its own (e.g., a C-Corp or an LLC taxed as a corporation).

In contrast, if your LLC is a disregarded entity and in Spain is considered under the rental income attribution (RIA) regime, it lacks its own tax personality and can't be considered a tax resident in Spain.

In that case, the effective management has no legal effect on the entity, and taxation falls directly on the partner through IRPF.

✅ LLC Disregarded (Transparente)

Since it lacks its own tax personality (you're the taxpayer, not the company), the entity's effective management technically has no legal effect. Taxation falls on the partner via IRPF

❌ C-Corp / Opaca (Contribuyente)

If the entity is taxed on its own and you're managing it from your couch in Spain, the Spanish tax authority will apply the law to consider it fiscally resident here and charge Corporate Tax.

🧾 What does the law say if the LLC isn't pass-through?

Practically speaking, effective management only matters if the entity is taxed independently. That is, if your LLC:

- ❌ Wasn't incorporated under Spanish law

- ❌ Doesn't have its registered office in Spain

- ✅ But you manage everything from Spain and the LLC is taxed as a corporation (C-Corp), the tax authority might consider it fiscally resident in Spain (art. 8.1.c LIS).

“An entity is considered fiscally resident in Spain when it has its effective management seat in Spanish territory. Effective management is understood to exist when the management and control of its activities are located in Spain.”

🎯 Control vs Ownership: It's not the same as being the owner or being in charge

"The day the IRS asks you who's in charge here, you'd better have an answer that isn't you."

This is the most important concept in this guide. If you understand it, everything else falls into place.

Imagine you buy an apartment building. You're the owner (proprietor). But you don't paint the walls, fix pipes, or collect rent. For that, you hire a property manager. You decide whether to sell the building or raise rents. They execute, sign, comply, and manage day-to-day.

Your LLC funciona exactamente igual:

👤 Tu = Member (Dueno)

- You are the 100% owner of the LLC

- You decide the strategy: what you sell, to whom, for how much

- You receive profits (distributions)

- Live wherever you want: U.S., Latam, Asia…

⚙ Manager (U.S. Administrator)

- U.S. citizen with U.S. domicile

- Signs documents, responds to the IRS, manages compliance

- Authorizes distributions of profits

- You make day-to-day operational decisions

👥 Roles within your LLC

Why does it matter to know who's who? If the Spanish tax authority inspects you, they'll ask: «Who decides?», «Who signs?», «Who executes?». Each role has a specific function in the defense narrative:

You — Member / Operational Scout

Owner and productive driver. You identify opportunities, propose operations, and execute what generates value (or delegate to freelancers). Your proposals require approval from the Manager. You produce, the Manager authorizes.

Manager (Devil Club LLC)

Executive decision-making capacity. Manages the LLC from the U.S.: signs, compliance, IRS, bookkeeping, and authorizes distributions. The person who «calls the shots» on paper.

Authorized Representative

Authorized person to act on behalf of the LLC with banks or specific institutions (e.g., opening an account with Mercury).

📚 The OA: Where it's written who calls the shots

All this is formalized in the Operating Agreement. It's not a generic document — it's designed so that the Member (you) do not appear as the one controlling the LLC. The Manager has executive power. Some key clauses:

📋 The Governance System: Every Decision Leaves a Trail

At Devil Club, we use a system we call Governance Ledger (governance ledger). It sounds technical, but in practice, it's simple: each decision requiring Manager authorization is documented with date, signature, and reference number.

Every request that goes through the Manager (distribution, contribution, contract, investment) gets a verifiable unique code. It's the governance trail of your LLC.

When the Manager approves a distribution or makes a key decision, they sign a Manager Resolution. It's a formal record of the decision.

Quarterly and annual. Summary of operations, distributions, and LLC status. If the IRS asks, you show them the report.

🔒 Your Biggest Enemy Isn't the Tax Authority: The 7 Mistakes That Destroy Your LLC

The Solution: Manager Service for Your LLC (Your 'Proof of Life' to the Spanish Tax Authority) 🛡

If your LLC is transparent (disregarded), the tax authority won't try to claim that 'the company lives in Spain.' Since you're already taxed on your IRPF, that's not a concern for them.

Their real attack is much more dangerous: Simulation. The tax authority will try to prove that your LLC is a 'paper company' or a 'shell company.' They'll claim that since you're doing everything from your home couch, the LLC doesn't have real activity in the U.S. and is just a trick to deduct expenses or move money.

This is where our U.S. Manager service becomes your best defense.

Why do you need a Manager if you're 'already paying' in Spain?

For a company to be respected, it must have economic substance. If you're the only one signing, moving funds, and making decisions, the company is you, not the LLC.

A Manager breaks that total control and provides the reality that the tax authority hates:

We act as your company's operational platform. We handle legal compliance, bank solvency, and supplier validation directly from the U.S., ensuring the company's administrative 'heart' beats outside of Spain.

The entire relationship is formalized through a service contract between your LLC and our entity (a U.S. Person with real operational headquarters).

- Documents that executive management occurs outside of Spain.

- It's tangible proof of substance in the face of inspections or requirements.

- ✓ IRS: Forms 5472 and 1120

- ✓ FinCEN: Reporte BOI

- ✓ BEA: Encuesta BE-13

- ✓ FinCEN: Reporte FBAR-114

A generic OA downloaded from the internet is a 3-page form that doesn't protect anything. Ours is a legal document with:

- Devil Club as designated Manager with real executive authority

- Defined powers: contract signing, account opening, expense approval

- Explicit limitations: asset sales, debts, structural changes require your approval

- Documented and auditable decision-making processes

- Indemnification clauses and owner protection

- Exit and dissolution procedures without legal gaps

The tax authority's question isn't «How much do you invoice?». It's «Who's in charge?». The Manager disrupts that narrative:

- Documented management from the U.S.: Executive decisions with traceable records

- Governance control: The Manager checks solvency before authorizing documents

- Real separation: You propose strategy, the Manager executes visible operations

- Binding veto: If an instruction compromises the LLC, the Manager vetoes it

The Operating Agreement states how governance should work. The Manager executes it. The Ledger records its execution:

- Total traceability: Each documented authorization with verifiable cryptographic hash

- Cryptographically verifiable: SHA-256 hash per resolution, unalterable history

- Cumulative history: Years of documented governance = accumulated corporate evidence

- Public verification: Any verifiable resolution en devil.club/verify

Every contract you personally sign is a bullet against your own structure. When the IRS sees Devil Club LLC, Manager of [Your LLC], they see an independent entity:

- Personal-corporate separation: The LLC acts as an autonomous entity

- Providers and tools: Signed by the Manager, not you

- Acuerdos comerciales: Partnerships, NDAs — la LLC es la parte

- Ledger recording: Each contract documented with date and reference

All members have Bookkeeping Basic: synced transactions, KPIs, and reclassification. With Manager, bookkeeping steps up:

- U.S. books: Accounting records under Manager custody in the United States

- Bank sync: Mercury and Wise connected — each transaction classified in real-time

- Professional PDF reports: Monthly, quarterly, and annual reports with tax narrative

- Tax Filing foundation: Numbers directly feed into forms 5472 + 1120

Your LLC doesn't pay taxes in the U.S. — but it's required to report. Tax Filing is proof that your company complies:

- Form 5472: Transactions between the LLC and its foreign owner

- Pro-forma 1120: Informative corporate return — no payment generated

- Powered by Bookkeeping: Numbers come from Manager's accounting

- Managed deadlines: Manager files on time. No surprises

A real company doesn't just operate — it analyzes, decides, and documents. Lucy is the AI in the Manager ecosystem: she uses 5 real data sources to generate proactive governance:

- Monthly, quarterly, and annual reports: Written in a human voice, citing real numbers and comparing to previous periods

- Health Score (0–100): Compliance, finances, profile, and engagement — at a glance, you know how your LLC is doing

- Proactive proposals: Every week, Lucy suggests concrete actions you can approve or reject from your dashboard

- Ledger-sealed: Each recorded decision is sealed with SHA-256, verifiable at devil.club/verify

- Adaptive persona: Lucy learns from your decisions, your industry, risk tolerance, and stated goals

Each time you access the panel, the system automatically logs your country of origin. Without lifting a finger, you build a verifiable map of your presence by country that complements your file in case of a tax inspection.

- Passive tracking: Activated with each login. No additional steps required

- Annual calendar: Monthly view with country color codes and source indicator (auto / manual / inferred)

- 183-day alerts: Notification when you approach the threshold that triggers tax residency in most jurisdictions

- Exportable: PDF report to attach to your file or deliver to your advisor

The previous 7 tools generate evidence over years. The Dossier is the complete dump of everything — organized, sealed, and ready for your tax advisor to evaluate and use:

- §1 Foundational Structure: Current OA, designated Manager, defined executive powers

- §2 Executive Authority: Management Contract, formal designation, effective date

- §3 Governance History: All Ledger resolutions with verifiable SHA-256 hashes

- §4 Contractual Activity: Contracts signed by the Manager on behalf of your LLC

- §5 Financial Substance: Accounting summary, income/expenses, synced bank

- §6 US Tax Compliance: Form 5472 + Pro Forma 1120 filed

- §7 Proactive Governance: Strategic reports, approved decisions, directives

Automatically generated, organized by year, with index, professional cover, and cryptographic seal. Your advisor receives a 100+ page PDF with all the organized evidence. No improvising, no searching for papers — working with real data.

The previous 8 tools generate data, documents, and evidence. The API gives you direct access to everything from your own code:

- 7 endpoints REST: /v1/bookkeeping, /v1/ledger, /v1/documents, /v1/entity, /v1/profile, /v1/reports, /v1/payments

- 12 granular scopes: control exactly what each API key can do

- Bearer token authentication: API keys in dc_live_xxx format, SHA-256 in DB

- Security: IP whitelisting, rate limiting (100 req/hr), configurable expiration

- Audit log: each call is logged with IP, timestamp, and used scope

Ideal for technical clients who want to automate bookkeeping via Mercury/Wise, build custom dashboards, or export data to external accounting software (Xero, QuickBooks). Your LLC, your data, your control.

- Generic MOI downloaded from the internet

- No Manager — the owner does everything

- No record of decisions

- You personally sign contracts

- No real bookkeeping — a hastily downloaded CSV

- Last-minute tax filing

- No AI or governance analysis

- Scattered evidence in emails and drives

- No programmatic access — everything manual

- Custom Operating Agreement with Manager, 15+ pages

- Devil Club como Manager ejecutivo

- Ledger with years of verifiable resolutions

- Contratos firmados por el Manager

- Bookkeeping sincronizado Mercury/Wise

- Professional tax filing derived from bookkeeping

- Lucy (IA) with proactive proposals sealed in Ledger

- Dossier de Evidencia Corporativa: todo consolidado en un PDF profesional

- Public API: full automation from your code

🔒 Tu Cortafuegos Legal: El Modelo de Gobernanza Corporativa

Devil Club's Management Contract and Operating Agreement establish a corporate governance model where the Manager (Devil Club LLC) exercises real executive authority over administration, treasury, and federal compliance of your LLC. Each corporate decision is recorded in a verifiable ledger. We explain how each mechanism works.

👥 El Modelo de Dos Roles

The structure separates functions into two roles with clearly defined competencies by contract:

🏛 Designated Manager (Devil Club LLC)

- Exclusive executive authority over administration, treasury, and federal compliance

- Mandatory ratification or veto on contracts >$1,000 USD

- Prior authorization for distributions, transfers >$10,000, and financial commitments >$10,000

- Execution of solvency stress-tests before each distribution

- Binding veto if an operation compromises financial viability or tax compliance

- Maintenance of corporate books and records in the U.S.

- Management of federal obligations (IRS, forms, compliance)

🔍 Operational Scout (You, the Member)

- Identification of business opportunities, customers, and suppliers

- Proposal of business operations to the Manager for ratification

- Day-to-day operational execution within authorized limits

- Solicitud formal de distribuciones de beneficios

- No authority to commit the LLC to contracts >$1,000 without Manager approval

- No ability to interfere with federal compliance decisions

This separation is not rhetorical. The agreement states that all decisions made under this framework are considered corporate decisions made under the jurisdiction of New Mexico. The Manager operates from the U.S. and exercises authority from U.S. territory.

Clause: Executive Ratification & Veto Power

Any contract, agreement, or commitment exceeding $1,000 USD requires the Manager's digital signature or approval to be valid. Without this ratification, the act does not bind the LLC.

The Member acts as Operational Scout: identifies the opportunity, negotiates preliminary terms, and presents the operation to the Manager. The Manager evaluates the operation from a financial viability and compliance perspective and issues their ratification or veto.

What does this mean in practice? The LLC cannot assume significant obligations without an executive decision made from the U.S. This generates a real and documented governance flow for each relevant operation.

Clause: Treasury Management & Solvency Lock

Before authorizing any distribution of profits to a Member, the Manager runs a Solvency Stress-Test. This test verifies that the LLC maintains sufficient liquidity to:

- Cover outstanding federal and state tax obligations

- Maintain an operating cushion for recurring expenses

- Not compromise the entity's financial viability

If the stress-test determines that funds are insufficient, the Manager issues a binding veto blocking the distribution. The Member cannot force a distribution vetoed by the Manager.

This mechanism protects the LLC's financial integrity and prevents piercing the corporate veil. If corporate funds are treated as the owner's personal account, limited liability protection weakens. The Solvency Lock ensures this doesn't happen.

Clause: Treasury Authorization Policy

The Management Contract requires prior explicit Manager authorization for the following transactions:

This policy ensures that significant financial movements of the LLC go through an independent executive filter, operating from the U.S.

Clause: Governance Ledger (Operating Agreement)

Each executive action by the Manager — ratifications, vetoes, treasury authorizations, stress-test results — is recorded in the Governance Ledger, a digital corporate minutes book.

How does SHA-256 verification work?

- Each ledger entry generates a unique SHA-256 cryptographic hash based on its content (date, action, parties, result).

- This hash acts as a digital fingerprint: if someone modifies a single comma in the record, the hash changes and the tampering is exposed.

- Hashes are chained sequentially, so each entry references the previous one. This creates a verifiable integrity chain.

- The result is a corporate record that can be mathematically audited: any third party (auditor, tax authority, court) can verify that the records have not been altered.

The Governance Ledger is not decorative. It's the documentary proof that each corporate decision was made following the governance protocols established in the Operating Agreement, with complete traceability from request to resolution.

Clause: Non-Interference Protocol

The contract explicitly states that the Member cannot interfere with the Manager's decisions regarding federal compliance, tax policy, or corporate administration.

If the Manager determines that a Member instruction compromises the LLC's financial viability or compliance with U.S. regulations, the Manager is contractually obligated to veto that instruction.

This creates a clear governance hierarchy: compliance with U.S. federal law takes precedence over owner instructions. The Manager is not an order executor — they're an independent fiduciary.

The Manager reserves the explicit right to freeze or reject distributions if the LLC lacks sufficient liquidity to meet its U.S. tax obligations. This clause exists specifically to prevent piercing the corporate veil.

“The Manager reserves the EXPLICIT RIGHT TO FREEZE OR REJECT distributions if the Company lacks sufficient liquidity for US tax obligations... prevent piercing the corporate veil.”

This mechanism ensures that LLC funds are treated as corporate funds subject to governance, not as the owner's personal assets. The distinction is legally determinative.

🏛 Sustancia Corporativa Real vs. Estructuras de Papel

The fundamental difference between the Devil Club model and services that simply 'register an LLC' is the operational substance:

❌ Structure without real governance

- The LLC is registered with a Registered Agent

- The owner makes all decisions unilaterally

- No controls over distributions or financial movements

- No record of minutes or decision traceability

- The books are kept (or not) by the owner from their country

- The 'substance in the U.S.' is reduced to a mailing address

✅ Modelo Devil Club (Manager-Managed)

- Manager with real executive authority operating from the U.S.

- Contracts >$1K require executive ratification

- Distributions subject to Solvency Stress-Test and authorization

- Governance Ledger with SHA-256 cryptographic verification

- Books and records maintained in the U.S. by the Manager

- Manager's binding veto on operations that compromise compliance

- All corporate decisions under New Mexico jurisdiction

Corporate substance doesn't depend on where the owner lives. It depends on where executive decisions are made, where records are kept, and who exercises fiduciary authority. In the Devil Club model, these three functions reside in the U.S.

Protection doesn't come from a document stored in a drawer. It comes from a governance system that operates continuously:

- Each relevant transaction passes through an executive filter in the U.S. before execution. This generates continuous documentary evidence of economic substance and real governance.

- The Governance Ledger creates an immutable record of corporate decisions. It's not a static document: it updates with every Manager action and is cryptographically verifiable.

- Solvency Lock provides documentary governance control over distributions. Fund withdrawals require formal authorization after a solvency stress test —the Manager doesn't hold funds, but signs and registers authorization.

- The Non-Interference Protocol establishes a legal hierarchy where federal compliance prevails over owner instructions. This is authentic corporate governance.

The governance system works because it's used. Request distributions formally. Send operations for ratification. Don't make relevant transfers without Manager authorization. Each processed request, each veto issued, each stress test executed is another entry in the Governance Ledger —and another piece of evidence that your LLC's corporate governance is real and operates from the U.S.

📜 Your LLC's Operating Agreement: What It Is and Why You Need It

The Operating Agreement (OA) is the fundamental internal document that regulates the operation and management of your LLC.

Although it's not mandatory to file it in many U.S. states, its correct drafting is key to establishing a solid structure, defining roles, and ensuring legal security for your global business.

What Is It Really For?

If you want to strengthen the economic substance of your LLC and professionalize your structure, an OA helps formalize the delegation of functions to a professional manager.

A well-structured OA with a manager includes:

- 🔹 Administrative Delegation: The manager handles legal compliance in the U.S., ensuring the LLC adheres to local statutes and regulations.

- 🔹 Role Clarity: Defines the manager's day-to-day operations and compliance, while you maintain strategic oversight.

- 🔹 Tax Compliance: The manager handles IRS obligations (official forms), taking that burden off you.

⚖ Importance for Your Legal Security

A well-drafted Operating Agreement and a professional Manager are key evidence that your LLC has real economic substance in its formation jurisdiction (the U.S.).

In short: The Operating Agreement is the legal backbone of your LLC. When properly designed, it allows you to operate transparently and have structured documentation in case of any information request.

📑 Basic Anatomy of an Operating Agreement

A professional Operating Agreement for a Single-Member LLC usually includes these sections:

Name, state, business purpose

100% ownership, capital

Manager-managed, delegation

Withdrawals with authorization

Books, records, fiscal year

Closure, transfer, inheritance

NM jurisdiction, indemnification

Clients on the Manager plan can customize their Operating Agreement through a step-by-step wizard. Activate optional clauses, configure variable data, and generate a verifiable PDF:

- 🔹 Succession and inheritance: Designate an automatic beneficiary.

- 🔹 Intellectual Property: Assigns all IP to the LLC.

- 🔹 Confidentiality (NDA): Built-in Member-Manager agreement.

- 🔹 POA for the IRS: Limited power of attorney (Form 2848).

- 🔹 Distributions and reserves: Distribution frequency and reserve account.

- 🔹 Tax election: Explicit statement as a Disregarded Entity.

«…must not only be, but also seem to be».

Heads up: Naming a Manager in the Operating Agreement isn't a magic shield if reality says otherwise. It's just another leg on the table.

For your structure to hold up, management must be genuine. If the agreement says a Manager in New Mexico is in charge, but the Spanish tax authority sees you making all the decisions, signing everything, and operating from Spain, reality (substance) trumps paperwork (form). Use it consistently.

🔒 Operating Agreement “Anatomy of Your Deterrent”

Your LLC's Operating Agreement is designed to establish a real corporate governance framework. Each clause serves a specific function in creating corporate substance in the U.S. We analyze the most relevant ones here.

All administrative, financial, and compliance management is formally delegated to Devil Club LLC as Manager, operating from the U.S.

The Member is limited to the role of Operational Scout: identifying opportunities, proposing operations, and executing tasks within the limits authorized by the Manager. Executive decisions—ratifying contracts, authorizing significant expenses, managing federal compliance—are the exclusive competence of the Manager.

Practical implication: There is a formal chain of command where executive authority resides in the United States. The Member cannot commit the LLC to significant operations without Manager approval.

The Operating Agreement states that the LLC's corporate books and records are maintained in the U.S. under the custody of the Manager.

This includes the Governance Ledger (record of corporate decisions with SHA-256 verification), authorized distribution records, Solvency Stress-Test results, and federal compliance documentation.

Practical implication: Corporate accounting and governance records are located in the U.S. and managed by the Manager. The Manager, assisted by Lucy (AI), issues annual reports and periodic communications to the Member about the LLC's status.

Distributions of profits to the Member are not automatic or unilateral. They require:

- Formal request from the Member to the Manager.

- Solvency Stress-Test executed by the Manager to verify that the LLC maintains sufficient liquidity.

- Explicit authorization from the Manager, who can veto distributions if they compromise tax obligations or financial viability.

Practical implication: LLC distributions are subject to documentary governance oversight. The Manager defines authorization procedures, runs solvency stress-tests, and signs off on approvals, but does not hold funds or act as a trustee for assets. This establishes that corporate withdrawals are not made at the owner's discretion, but are governed by executive protocols from the U.S.

Executive delegation, record-keeping in the U.S., and governance oversight of distribution authorizations are not decorative clauses — they're the pillars of a continuously operating governance model. The key is to use the protocols: formally request distributions, submit transactions for ratification, and allow the governance system to generate the documentary record that supports the substance of your LLC.

💶 Taxes, the Spanish tax authority, and Your LLC's Taxation

How to optimize, comply, and bring the money home without unnecessary 'gifts'.

🏛️ IRPF and U.S. LLC: Income Attribution according to the tax authority

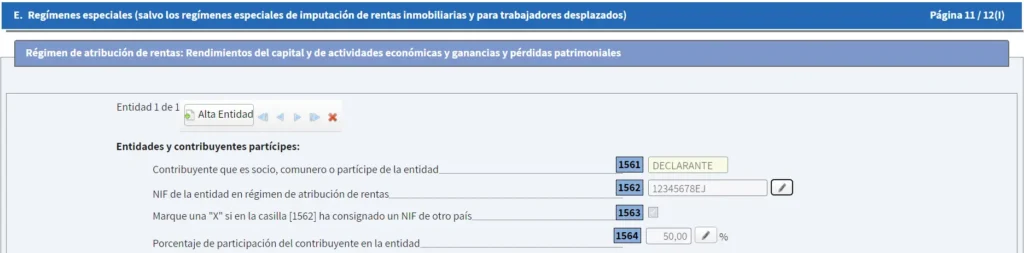

Entities in the income attribution regime (RAR) don't pay taxes as an entity. Instead, their income is distributed to their members, who report it on their individual tax returns. 📋

This also applies to some foreign entities, like U.S. Single Member Disregarded LLCs operating in Spain and taxed equivalently. 🌐

The issue with Model 100 in LLCs

Is this legal? To put minds at ease, we went straight to the source. We asked the Spanish tax authority to confirm the tax regime and, while we had them, asked for explanations about the infamous 'bug'.

The error occurs when you're declaring these returns:

- The form asks for your participation percentage in the entity.

- But it only lets you enter up to 99%, even if you're the sole owner (100%).

- The form automatically calculates the income to report as:

Fecha: 02/07/2024

❓ The Citizen's Question

I'm a Spanish tax resident and sole owner (100%) of a disregarded U.S. LLC. When trying to file Model 100, the program only allows me to enter 99% participation. How should I report?

📢 Administration's Response (Literal)

Yes, it's Income Attribution:

Report in Model 100, Section E, as “economic activity income”.

On the Software Glitch (The Bug):

“The fact that the assistance program doesn't allow 100% entry in this particular case shouldn't undermine the previous obligation. What's relevant is including all income.”

📄 Official AEAT response dated 2024-07-02 — available on request through the AEAT Electronic Office.

🧮 Real Calculation Example (2026 Income Tax in Catalonia)

Assume your LLC generates $60,000 in revenue this year and has $15,000 in deductible expenses. This results in $45,000 in net profit, which, as a pass-through entity, is directly attributed to you as the sole member.

This means you must report that $45,000 in Spain, on your Income Tax Return, under the «Attribution of Income Regime» section. The LLC itself does not pay taxes in the U.S.; it only files informational reports using Form 5472 and a pro-forma 1120.

❌ Your LLC does NOT pay tax in the U.S.

Only files informational reports (Form 5472 + pro-forma 1120). No federal taxes.

✅ YOU pay tax in Spain

Reports income on your Income Tax Return as «foreign economic activity income», applying current tax brackets.

🧾 Calculadora Tramos IRPF 2026

| Tramo de Renta | Estatal | Regional | Total | Cuota Tramo | Acumulado |

|---|

🔒 Club: 99% Hack (Free Bug Solution)

The Master Formula

The goal is to inflate “Total Performance” so that, when you apply the mandatory 99%, the result is your exact real profit.

👇 Example with $100,000 in profit:

Don't put $100,000 and then 99%. You'd only be taxed on $99,000. That undeclared 1% is subject to penalties.

Don't try to hack the percentage field. The web program won't let you save. Use the formula.

If this gives you vertigo or your tax return is complex, don't risk it. We recommend using TaxDown (FULL Plan). They have their own software that sometimes allows adjustments the AEAT website doesn't.

📋 Documents you need to have ready:

If you're a Devil Club member with Manager service, you already have everything consolidated in your Corporate Evidence Dossier. This dossier includes:

- Complete bookkeeping: Income, expenses, and fiscal year balance.

- US tax returns: Form 1120 and Form 5472 filed with the IRS.

- Bank statements: Mercury, Wise, and other LLC accounts.

- Governance Ledger: Manager decisions and operations log.

- Invoices and contracts: Supporting documentation for deductible expenses.

If you don't have the Dossier, you'll need to gather each document separately (statements, accounting Excel, US tax returns, and invoices).

Plantilla Copy/Paste

📩 Text to send to TaxDown:

📩 Sample email to send to TaxDown:

Hi,

I have a US LLC as a single-member disregarded entity, and I'm a tax resident in Spain. I already have confirmation from the Spanish tax authority (DGT) that I can apply the income attribution regime in my personal tax return (IRPF).

I attach the Corporate Evidence Dossier prepared by my designated US Manager (Devil Club LLC), which includes:

• Complete bookkeeping for the year (income, expenses, balance).

• Filed US tax returns (Form 1120 + Form 5472).

• LLC bank statements.

• Governance Ledger.

• Supporting invoices and contracts.

I need your help with my personal tax return, including reporting the LLC's economic activity under the income attribution regime.

Let me know if you need anything else.

Thanks.

💸 Deductible expenses in an LLC: What you can and can't deduct

As we clarified earlier in the Myths section (Myth #1), if you have a US LLC (Limited Liability Company), you must include all business profits in your Spanish personal tax return (IRPF). This includes both amounts you withdraw and those you leave in the company. This way, you'll avoid issues with the tax authority and fulfill your tax obligations. 🇪🇸

Deductible expenses: Your only real tool

The key is to maximize deductible expenses. These are directly related to the business activity and are necessary and reasonable. By deducting them:

- 📉 You reduce the taxable base (the amount on which taxes are calculated)

- 💵 Pay less taxes

- 📈 Aumentas la rentabilidad neta

If you're unsure what you can deduct and what you can't, you may make serious accounting mistakes that lead to penalties. That's why it's crucial to understand the rules on deductible expenses, a topic we'll cover in detail below. 🙌

Here's the catch. The IRS is flexible, but you are taxed in Spain (IRPF). Spanish rules apply.

*Nota: In Spain, la carga de la prueba es tuya. Guarda agenda, emails y justificaciones de reuniones.

US Accounting: Keep it impeccable for your operations (Suppliers, SaaS, Banks).

Spanish Declaration: Filter and eliminate "flexible" IRS expenses that the tax authority won't accept.

Expectation: Your taxable base in Spain is usually higher than your real accounting profit in the U.S.

LLC deductible expense list

We created this Interactive Tool so you can stop guessing. Use filters to separate what's safe from what could get you audited.

Don't use your LLC as a personal piggy bank. Use this Expense Semaphore to filter your purchases.

Go ahead, without fear.

With care and perfect receipts.

Investments (amortized, not deducted at once).

🚦 Deductible Expense Semaphore

What the Spanish tax authority accepts and what it doesn't — IRPF Spain criteria

💸 How to bring money to Spain

Forget about “administrator payrolls”, IRPF withholdings on each invoice, and the hassle of Spanish LLC dividends. In a Single-Member LLC, company money is yours. The barrier is legal (liability), not financial.

🏛 En una S.L. Espanola

- You need payroll and social security.

- If you distribute profits (dividends), you pay taxes first at the company level (25%) and then personally (19-26%).